In his magisterial history of world power since 1500, The Rise and Fall of the Great Powers, which incidentally was the senior year graduation gift in 1988 that inspired me to become a professional historian—the Yale historian Paul Kennedy wrote that his work was not exclusively a military or economic history, but he wanted to “concentrate on the interaction between economics and strategy, as each of the leading states in the international system strove to enhance its wealth and power, to become (or to remain) both rich and strong.” Later in his book, reflecting on World War II, Kennedy wrote that “Clearly, economic power was never the only influence upon military effectiveness, even in the mechanized, total war of 1939-1945.” Kennedy put forward the following analysis: “Economics, to paraphrase Clausewitz, stood in about the same relationship to combat as the craft of the swordsmith to the art of fencing.” In other words, superior economic and technological strength forged the means to fight and superior numbers could provide an advantage for victory, but war material could not substitute for actual performance in the hands of warriors on the battlefield.

The battle that I would like to discuss focused on the interaction between economics and empires. It began on the last day of June 1944, when conference guests began arriving to a quiet and recently refurbished 234 room resort hotel named the Mount Washington, deep in the White Mountains of New Hampshire. The United Nations Monetary and Financial Conference, which would become known as the Bretton Woods conference for the agreement reached there, saw the representatives of 44 nations, including the Soviet Union and China, gather to create a new postwar international monetary system.

For the 730 attendees, the stakes could not have been higher. The economic experts believed that the task of preventing a Third World War was ultimately in their hands. The previous thirty years of history weighed on them. From the Versailles peace, they knew intimately how deeply indebted nations became radicalized. They knew that the attempts to reinstall the gold standard, which had ended in 1914, had bred international financial instability through the 1920s. They knew the fascist infection strengthened on economic insecurities, and the global depression which engulfed the 1930s made aggressive militarism an attractive and effective pathway to solve economic problems like unemployment and lack of natural resources. Now, in the crux of escalating war, they were there to break the vicious cycle. What is fascinating about what one author has called “The Battle of Bretton Woods” is that it was primarily fought between two Allied nations whose troops were literally dying together in Normandy, Italy, on the seas and in the Far East: the United Kingdom and the United States. In truth, Bretton Woods was actually the end of a confusing campaign between a faltering British Empire and a somewhat reluctant, rising American one. And the story of how the Allies came to the agreement is rife with ironies.

While we don’t have time to recite the interwar history of the gold standard, it is important to note that there was bad blood between the two Anglo nations over the issue. Britain had abandoned the international gold standard in 1931. An important detail for what would transpire at Bretton Woods, however, is that while the pound sterling lost its “peg,” or set price, to gold, the pound remained “pegged” to other currencies within the British Commonwealth nations, who could expect stable exchange rates for sterling as part of the Imperial Preference system. When the London Economic Conference was held in 1933 with the aim of re-establishing stable exchange rates for the pound and dollar based on the gold standard, President Franklin Roosevelt torpedoed the conference, declaring: “I would regard it as a catastrophe amounting to a world tragedy if the greatest conference of nations, called to bring about a real and permanent financial stability . . . allowed itself a purely artificial and temporary expedient . . .” Through an Executive Order, FDR “nationalized” gold, meaning all American supplies in private hands had to be handed over to the US Treasury at a lower price ($20.67) than the current market ($29.62). FDR wanted to devalue the dollar, so he was against any “peg” to gold.

Ironically, however with this act and an upward turn of the US economy in late 1933, the purchasing power of the dollar rose. By 1934, gold stabilized at about $35 an ounce, where it roughly remained a decade later when the delegates fought out their draft proposals at conference tables and the bar at Bretton Woods. I am certain that that number sounds familiar to many of you today, because the most important takeaway that most people know about the Bretton Woods conference is that the United States agreed to purchase gold at $35 an ounce for the postwar future—in other words, we agreed to “peg” the dollar to gold, and allow other national currencies to “float” their values against the dollar.

Here is something, however, I bet most people don’t know: the first formal plan to reform the postwar international monetary system was not proposed by Britain or America. It was put forward by Nazi Germany. In July 1940, after the defeat of France, Hitler’s Minister of Economics Walter Funk unveiled the German plan for a financial “New Order” across the Nazi Empire. The plan was actually sophisticated: gold’s importance was essentially eliminated, with other national currencies floating against each other; nations outside the Nazi system would have to balance their exports and imports with the Nazi system; and payments would be channeled through a clearing house in Berlin. As historian Ed Conway puts it, if one squints, you can see an “early blueprint” of the modern European Union.

Because this was a serious proposal, Harold Nicolson in the British Ministry of Information forwarded the plan to the most eminent economist of the day, John Maynard Keynes, and asked him to discredit it. Keynes, never one to read from a pre-arranged script, instead declared that, quote: “In my opinion about three quarters of the passages quoted from the German broadcasts would be quite excellent if the name of Great Britain were substituted for Germany . . . If Funk’s plan is taken at face value, it is excellent and just what we ourselves should be thinking of doing.” This exchange forced Keynes and the British to put some deep thought into what a postwar monetary order should look like. Of course, Keynes was world famous as the economist who had ripped the Versailles treaty to shreds with his 1919 polemic The Economic Consequences of the Peace. In that work, he had savaged the deep debts that had been imposed on Germany. Here’s an irony, however, that Keynes had to confront in 1940, and which would deeply impact how the Bretton Woods conference would play out four years later: in World War II, Britain was a debtor nation.

Another irony was that Keynes, who had unabashedly cheered FDR in 1933 when the President sought to destroy the gold standard, now began to formulate postwar plans based upon the Nazi vision, but with an enhanced role for gold in the system. Keynes’ vision of the postwar world centered upon what he initially called a European Reconstruction Fund, which became the World Bank at the Bretton Woods conference, and which would provide for long-term economic investment and growth amongst member nations. As a debtor nation who desired to hold onto her “sterling sphere” in the postwar world, Britain’s great postwar monetary challenge was to prevent the outflow of gold and sterling from the Bank of England. Here is where the perennial question of an individual’s impact upon history always comes up. John Maynard Keynes was known as a maverick thinker, a brilliant Cambridge don, tall and piercingly charismatic. He was revered as a prophet for his condemnation of Versailles, and held in awe as a theoretical economist for his 1936 explanations of capitalist economics in The General Theory of Employment, Interest and Money. No less than the philosopher Bertrand Russell said that he felt that he took his own life in his hands whenever he debated Keynes, because Keynes was so analytical and persuasive. Despite health problems, in 1944 Keynes agreed to lead the British delegation at Bretton Woods.

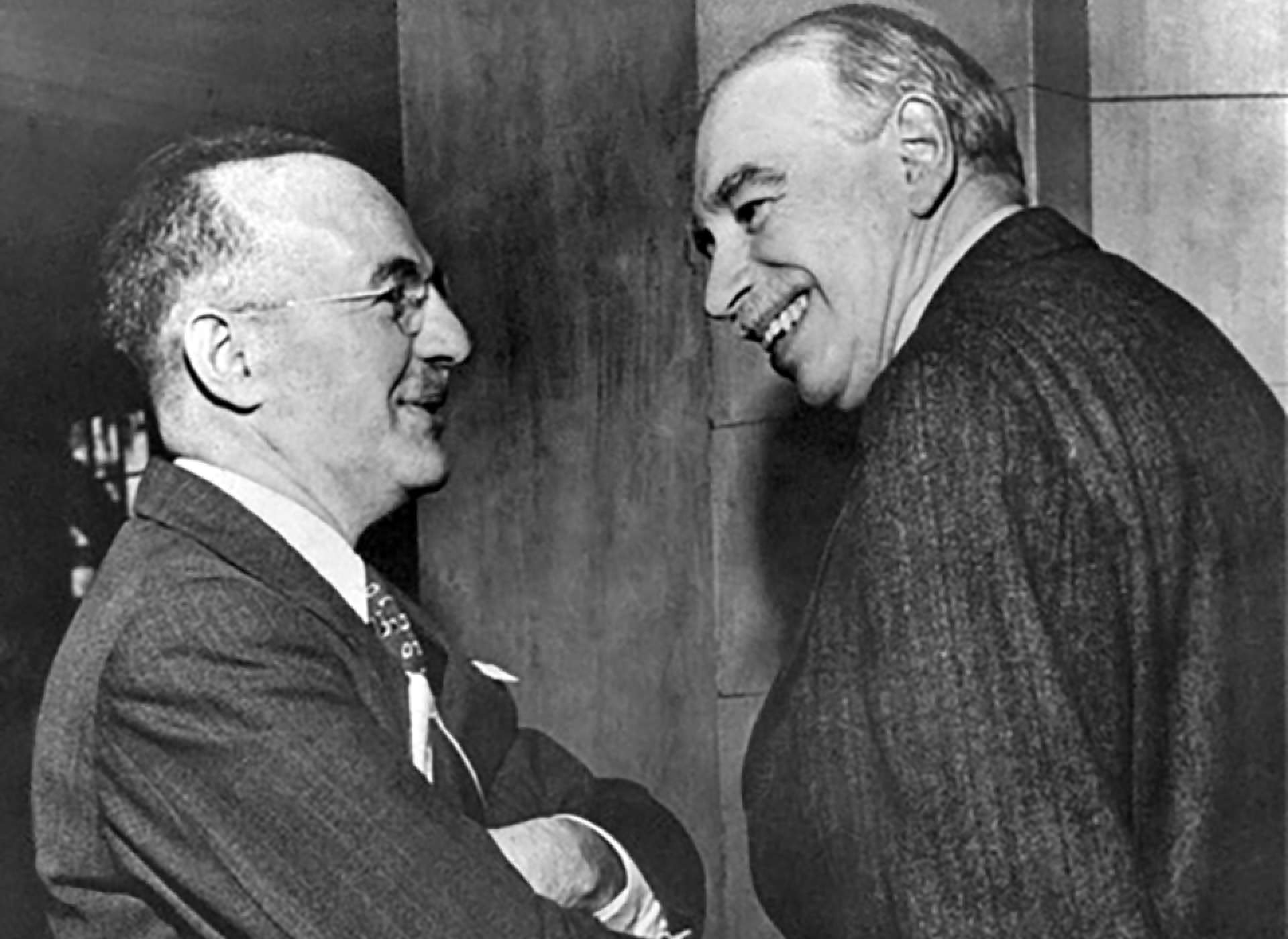

Harry Dexter White and John Maynard Keynes at Bretton Woods, July 1944

But for all his brilliance, Keynes could not overcome the fact that Britain was a debtor nation, and the United States was a creditor nation. The conference at Bretton Woods was in fact controlled by a US Treasury bureaucrat, Dr. Harry Dexter White. White was the polar opposite of Keynes: short, Jewish, with a round face and glasses, and known to be so rude that future Secretary of State Dean Acheson later said that when White was accused of being a communist, he himself had hurled much worse names at White. Even before Pearl Harbor, White began working on his own vision of a postwar monetary order. The particulars in his plan generally tracked Keynes’ own ideas. There was one major difference, however: White’s vision of a monetary clearing house, which he called the International Monetary Fund (or IMF), would perform the functions of a central banker by controlling capital flows within the international system. White’s vision sought to eliminate what had previously been recognized as a gold standard system, but kept the US dollar at the center of the system.

By contrast, Keynes envisioned the creation of a new international currency he called the Bancor to facilitate currency exchanges for the proposed IMF—one can glimpse today’s Euro in the idea. But he also had the task of protecting the Imperial Preference system with London as its financial center. Representing a debtor nation, Keynes viewed any agreement to “peg” the price of gold, whether by an international body or the Bank of England, as financially fatal to the British Empire. This is basically where matters stood on the last day in June 1944 when the delegates gathered at Bretton Woods. Many delegates had sons who were fighting, and worried that bad news would arrive during the three weeks of the conference. Before the actual conference began, the American and British delegations met in Atlantic City to compromise their visions where they could. It was agreed that White would chair Commission I, which created the International Monetary Fund, while Keynes would chair Commission II, which created the World Bank.

But while the Anglo-American alliance commanded the proceedings for the next three weeks in July, the realities of the interaction between economics and empires actually shaped the outcomes more than their best-laid plans. Foremost was the financial reality that the United States was a creditor nation, and Britain was a debtor nation. Although Keynes was personally treated as a rock star throughout the conference, the less charismatic White controlled the most important proceedings in shaping the International Monetary Fund, which clearly emerged over the World Bank as the more powerful monetary institution. Keynes knew the temper of the conference, and that there was opposition to his idea of the Bancor as an international currency. However, White had deliberately inserted in the IMF drafts a benign phrase, “gold and gold-convertible exchange,” whenever a particular unit of account was needed. The key moment that shaped the Bretton Woods agreement came when A.D. Shroff of the Indian delegation, concerned about the convertability of rupees to the pound sterling in the Imperial Preference system, asked that the American delegation give a precise definition of what “gold and gold-convertible exchange” was.

In response, a member of the British delegation, the respected economist Dennis Robertson, proposed that “payment of official gold and subscription should be expressed official holdings of gold and United States dollars.” It should be noted that this was not a simple mistake on Robertson’s part—the next day he checked to make certain that “gold and United States dollars” was included in the document text. This situation is rife with ironies. First, despite Keynes’s best efforts, it was a fissure within the British Empire with India that brought the issue of the role of the dollar in the new system up for decision. Second, in an even greater irony, it was a member of the British delegation who understood that the dollar was the sole currency which had the strength and stability to be exchanged for gold. It was not the Americans who proposed to put the dollar at the center of the postwar world economy. Instead, it came through the weakness of the British Empire, fracturing in two places: first, through the surging national independence of India, seeking to protect her own economic interests; and second, through the weakness of an indebted Britain and Bank of England, who could no longer provide stable exchange rates. The only option was to anchor the international monetary system to the one currency that could: the US dollar.

There is one other irony in the power play between empires that was happening at Bretton Woods, involving the rising military empire of the Soviet Union. As I previously alluded, it goes to the intentions of Harry Dexter White. There is no doubt that White provided secret government documents on American financial plans and positions to the Soviet Union during the war. His motivations, and the extent of his betrayal, remain unclear to historians today: he never joined the Communist party, he viewed his own actions as aiding an ally during wartime, and his personal writings convey his economic vision of the future as a mixture of capitalism and socialism, rather than a Marxist faith. But shortly after White engineered the triumph of the dollar at Bretton Woods, in the fall of 1944 White became a passionate supporter of Secretary of Treasury Henry Morgenthau’s plan to turn industrial Germany into a pastureland. Keynes, it should be noted, was horrified by the Morgenthau Plan. White clearly understood that the Morgenthau Plan would decimate the postwar value of the German mark. With Soviet armies advancing across the battlefields of Europe, it appears that White thought that having eliminated the pound and mark as rivals, the Soviet ruble could fill the post-war financial vacuum, and eventually challenge the dollar.

Alas, it was not to be. Congress passed the Bretton Woods act in July 1945, legally pegging the dollar to gold. In December that year, Parliament passed Bretton Woods as a condition for receiving a loan from the United States which Keynes had desperately and bitterly negotiated. At the official Bretton Woods signing ceremony on December 27, 1945, the Soviet Union sent no delegates; White was shocked to learn that they would not sign. On February 9, 1946, Joseph Stalin declared “Marxists have more than once stated that the capitalist system of world economy contains the elements of a general crisis and military conflicts . . . As a result of this, the capitalist world is split into two hostile camps, and war breaks out between them.” Two weeks later, George F. Kennan sent his Long Telegram to the State Department, and on March 5, Winston Churchill declared at Fulton, Missouri that “from Stettin in the Baltic to Trieste in the Adriatic, an iron curtain has descended across the Continent.” The Cold War was on. Overworked during the war and suffering heart disease, John Maynard Keynes died in April 1946. Harry Dexter White’s influence within the Treasury department disintegrated under President Truman, who disliked the Morgenthau plan. In August 1948, three days after testifying before the House Un-American Activities Committee concerning his ties to the Communist spy ring exposed by Whittaker Chambers, White died of a heart attack.

The Bretton Woods conference in summer 1944 saw the global rise of the American Economic Empire—the empire of the dollar. It also saw the fatal financial strike which sealed the decline of the British Empire, and the foundation of the rising Soviet Empire upon military power and socialist economics, rather than international economics. After financing the resuscitation of the Free World, the Bretton Woods regime ended in 1971, when the US could no longer afford to pay $35 per ounce for gold. But in a final irony, we today know from Harry Dexter White’s papers that after his fall from influence, he came to believe that the $35 peg to gold, the hallmark of the Bretton Woods system, had been a mistake. He believed that the Bretton Woods international monetary system would survive much longer if in 1944 the US had instead pegged the dollar to gold at a price of $20.67-- the same price that FDR had “nationalized” gold in 1933.

This piece appeared originally as a presentation by Dr. Keith Huxen at the International Conference on World War II on November 23, 2019.

Keith Huxen

Keith is the former Senior Director of Research and History in the Institute for the Study of War and Democracy at The National WWII Museum.

Cite this article:

MLA Citation:

APA Citation:

Chicago Style Citation: